VIRTUS Protocol — Legal Disclosures

Effective Date: May 9, 2026

Version: 1.0

Table of Contents

REGULATORY STATEMENTS SUMMARY

PART I - INFORMATION ON RISKS

- I.1 Admission to Trading Risks

- I.2 Issuer-Related Risks

- I.3 Crypto-Assets-Related Risks

- I.4 Project Implementation-Related Risks

- I.5 Technology-Related Risks

- I.6 Mitigation Measures

PART D - INFORMATION ABOUT THE CRYPTO-ASSET PROJECT

- D.1 Crypto-asset Project Name

- D.2 Crypto-assets Name

- D.3 Abbreviation

- D.4 Crypto-asset Project Description

- D.5 Details of All Natural or Legal Persons Involved in the Implementation of the Crypto-asset Project

- D.6 Utility Token Classification

- D.7 Key Features of Goods/Services for Utility Token Projects

- D.8 Plans for the Token

- D.9 Resource Allocation

- D.10 Planned Use of Collected Funds or Crypto-Assets

PART E - INFORMATION ABOUT TRADING ADMISSION

- E.1 Public Offering or Admission to Trading

- E.2 Reasons for Public Offer or Admission to Trading

- E.3 Fundraising Target

- E.4 Minimum Subscription Goals

- E.5 Maximum Subscription Goal

- E.6 Oversubscription Acceptance

- E.7 Oversubscription Allocation

- E.8 Issue Price

- E.9 Official Currency or Any Other Crypto-assets Determining the Issue Price

- E.10 Subscription Fee

- E.11 Offer Price Determination Method

- E.12 Total Number of Offered/Traded Crypto-Assets

- E.13 Targeted Holders

- E.14 Holder Restrictions

- E.15 Reimbursement Notice

- E.16 Refund Mechanism

- E.17 Refund Timeline

- E.18 Offer Phases

- E.19 Early Purchase Discount

- E.20 Time-limited Offer

- E.21 Subscription Period Beginning

- E.22 Subscription Period End

- E.23 Safeguarding Arrangements for Offered Funds/Crypto-Assets

- E.24 Payment Methods for Crypto-Asset Purchase

- E.25 Value Transfer Methods for Reimbursement

- E.26 Right of Withdrawal

- E.27 Transfer of Purchased Crypto-Assets

- E.28 Transfer Time Schedule

- E.29 Purchaser's Technical Requirements

- E.30 Crypto-asset Service Provider (CASP) Name

- E.31 CASP Identifier

- E.32 Placement Form

- E.33 Trading Platforms Name

- E.34 Trading Platforms Market Identifier Code (MIC)

- E.35 Trading Platforms Access

- E.36 Involved Costs

- E.37 Offer Expenses

- E.38 Conflicts of Interest

- E.39 Applicable Law

- E.40 Competent Court

PART F - INFORMATION ABOUT THE CRYPTO-ASSETS

- F.1 Crypto-Asset Type

- F.2 Crypto-Asset Functionality

- F.3 Planned Application of Functionalities

- F.4 Type of White Paper

- F.5 The Type of Submission

- F.6 Crypto-Asset Characteristics

- F.7 Commercial Name or Trading Name

- F.8 Website of the Issuer

- F.9 Starting Date of Offer to the Public or Admission to Trading

- F.10 Publication Date

- F.11 Any Other Services Provided by the Issuer

- F.12 Identifier of Operator of the Trading Platform

- F.13 Language or Languages of the White Paper

- F.14 Digital Token Identifier Code

- F.15 Functionally Fungible Group Digital Token Identifier

- F.16 Voluntary Data Flag

- F.17 Personal Data Flag

- F.18 LEI Eligibility

- F.19 Home Member State

- F.20 Host Member States

PART G - RIGHTS AND OBLIGATIONS

- G.1 Purchaser Rights and Obligations

- G.2 Exercise of Rights and Obligations

- G.3 Conditions for Modifications of Rights and Obligations

- G.4 Future Public Offers

- G.5 Issuer Retained Crypto-Assets

- G.6 Utility Token Classification

- G.7 Key Features of Goods/Services of Utility Tokens

- G.8 Utility Tokens Redemption

- G.9 Non-Trading Request

- G.10 Crypto-Assets Purchase or Sale Modalities

- G.11 Crypto-Assets Transfer Restrictions

- G.12 Supply Adjustment Protocols

- G.13 Supply Adjustment Mechanisms

- G.14 Token Value Protection Schemes

- G.15 Token Value Protection Schemes Description

- G.16 Compensation Schemes

- G.17 Compensation Schemes Description

- G.18 Applicable Law

- G.19 Competent Court

PART H - UNDERLYING TECHNOLOGY

- H.1 Distributed Ledger Technology

- H.2 Protocols and Technical Standards

- H.3 Technology Used

- H.4 Consensus Mechanism

- H.5 Incentive Mechanisms and Applicable Fees

- H.6 Use of Distributed Ledger Technology

- H.7 DLT Functionality Description

- H.8 Audit

- H.9 Audit Outcome

PART J - SUSTAINABILITY INDICATORS

- J.01 Name

- J.02 Relevant Legal Entity Identifier

- J.03 Name of the Crypto-asset

- J.04 Consensus Mechanism

- J.05 Incentive Mechanisms and Applicable Fees

- J.06 Beginning of the Period to which the Disclosed Information Relates

- J.07 End of the Period to which the Disclosed Information Relates

- J.08 Energy Consumption

- J.09 Energy Consumption Sources and Methodologies

- J.10 Environmental Impact

ATTACHMENT 1 Preliminary Emission Schedule

ATTACHMENT 2 Distribution Model

| # | Field | Content |

|---|---|---|

| 01 | Date of notification | 05/03/2026 |

| 02 | Statement in accordance with Article 6(3) of Regulation (EU) 2023/1114 | This crypto-asset white paper has not been approved by any competent authority in any Member State of the European Union. The person seeking admission to trading of the crypto-asset is solely responsible for the content of this crypto-asset white paper. |

| 03 | Compliance statement in accordance with Article 6(6) of Regulation (EU) 2023/1114 | This crypto-asset white paper complies with Title II of Regulation (EU) 2023/1114 and, to the best of the knowledge of the management body, the information presented in the crypto-asset white paper is fair, clear and not misleading and the crypto-asset white paper makes no omission likely to affect its import. |

| 04 | Statement in accordance with Article 6(5), points (a), (b), (c) of Regulation (EU) 2023/1114 | The crypto-asset referred to in this white paper may lose its value in part or in full, may not always be transferable and may not be liquid. |

| 05 | Statement in accordance with Article 6(5), point (d) of Regulation (EU) 2023/1114 | FALSE |

| 06 | Statement in accordance with Article 6(5), points (e) and (f) of Regulation (EU) 2023/1114 | The crypto-asset referred to in this white paper is not covered by the investor compensation schemes under Directive 97/9/EC of the European Parliament and of the Council. The crypto-asset referred to in this white paper is not covered by the deposit guarantee schemes under Directive 2014/49/EU of the European Parliament and of the Council. |

SUMMARY

| # | Field | Content |

|---|---|---|

| 07 | Warning in accordance with Article 6(7), second subparagraph of Regulation (EU) 2023/1114 | Warning: This summary should be read as an introduction to the crypto-asset white paper. The prospective holder should base any decision to purchase this crypto-asset on the content of the crypto-asset white paper as a whole and not on the summary alone. The offer to the public of this crypto-asset does not constitute an offer or solicitation to purchase financial instruments and any such offer or solicitation can be made only by means of a prospectus or other offer documents pursuant to the applicable national law. This crypto-asset white paper does not constitute a prospectus as referred to in Regulation (EU) 2017/1129 of the European Parliament and of the Council (36) or any other offer document pursuant to Union or national law. |

| 08 | Characteristics of the crypto-asset | VRT is an ERC-20 token on Base blockchain that serves as the governance and incentive token for VIRTUS protocol. VIRTUS protocol is a next-generation automated market maker (AMM) designed to serve as Base blockchain's central liquidity hub. While VRT tokens are fully transferable and can be freely traded, they do not provide direct voting rights or fee-sharing benefits, as these privileges are only granted when VRT is locked for up to 4 years to receive veVRT NFTs (ERC-721 tokens). The VRT token has no intrinsic value or asset backing, deriving its worth entirely from protocol utility, with weekly emissions distributed to liquidity providers based on veVRT voting and a rebase mechanism that rewards veVRT holders proportionally to protocol growth. All functionalities are currently operational. |

| 09 | Services to which the Utility Tokens Give Access, Restrictions on Transferability | Not applicable |

| 10 | Key information about the offer to the public or admission to trading | VIRTUS protocol (the "Issuer") is seeking admission of VRT tokens to trading on Decentralized Exchanges, TBA on a later stage, (the "Trading Platform") to enhance liquidity and accessibility for protocol participants, thereby strengthening the ecosystem where liquidity providers, voters, and traders are fairly compensated through emissions and fee distribution. |

Part I – Information on Risks

I.1 Admission to Trading Risks

| # | Content |

|---|---|

| 1 | Increased price volatility: Exchange listing typically attracts new market participants including algorithmic traders, arbitrageurs, and short-term speculators who may not engage with the underlying protocol. This can lead to price movements disconnected from fundamental protocol metrics like TVL or fee generation. |

| 2 | Different trading environment: Centralized exchanges (CEXs) operate with order books, market makers, and different fee structures than AMM-based decentralized exchanges (DEXs). This creates potential for significant price discrepancies between venues, especially during volatile periods. Stop-loss hunting, liquidation cascades, and thin order books during off-peak hours can cause sharp price movements unique to CEX trading. |

| 3 | Platform operational risks: Exchange infrastructure issues such as matching engine failures, DDoS attacks, or scheduled maintenance can prevent trading access during critical moments. Platform insolvency, regulatory actions, or security breaches could result in frozen funds or trading halts. Users must trust the exchange's custody, unlike DEX's non-custodial nature. |

| 4 | Regulatory compliance: Trading platforms must comply with evolving regulations that may result in sudden delistings, geographic restrictions, or trading limitations. KYC/AML requirements may conflict with DeFi's permissionless ethos. Regulatory actions against the exchange could affect all listed assets regardless of individual compliance. |

| 5 | Market fragmentation: Price discovery becomes complex with liquidity split between CEX order books and multiple DEX pools. This fragmentation can be exploited by sophisticated traders at the expense of retail participants. Different fee structures, trading hours, and market mechanisms between venues create inefficiencies and confusion about market price. |

I.2 Issuer-Related Risks

| # | Content |

|---|---|

| 1 | Limited operating history: VIRTUS protocol was established in March 2026, and therefore there is limited historical performance data. |

| 2 | Evolving regulatory landscape: The VIRTUS protocol operates in an uncertain regulatory environment where DeFi governance tokens face potential reclassification as securities or other regulated instruments. Different jurisdictions are developing conflicting frameworks that could limit the VIRTUS Protocol's ability to operate globally. The VIRTUS protocol may need to implement geographic restrictions, modify token rights, or restructure entirely to comply with emerging regulations, potentially disrupting protocol operations. |

| 3 | Governance token holdings: The VIRTUS Protocol holds 100,000,000 VRT (50% of initial supply 200M VRT). These tokens are locked under the maximum lock duration ("Max Lock" mode), with the lock period continuously extended to ensure a permanent lock status. |

I.3 Crypto-Assets-Related Risks

| # | Content |

|---|---|

| 1 | Market-determined value: VRT derives value from protocol utility and market demand without underlying assets, revenue rights, or redemption guarantees. The token's worth depends on continued protocol usage, liquidity provider participation, and market interest, which can fluctuate significantly during market cycles. |

| 2 | Price volatility: VRT experiences substantial price movements characteristic of governance tokens, with potential daily fluctuations in double-digit percentages. Price correlates with Base TVL, DeFi sector trends, and broader cryptocurrency markets. Limited liquidity depth can amplify price movements. |

| 3 | Token model complexity: The dual-token system splitting VRT (liquid) and veVRT (locked NFT) requires careful understanding. Token holders should note that VRT alone does not provide voting rights or fee earnings. This complexity necessitates user education for informed participation. |

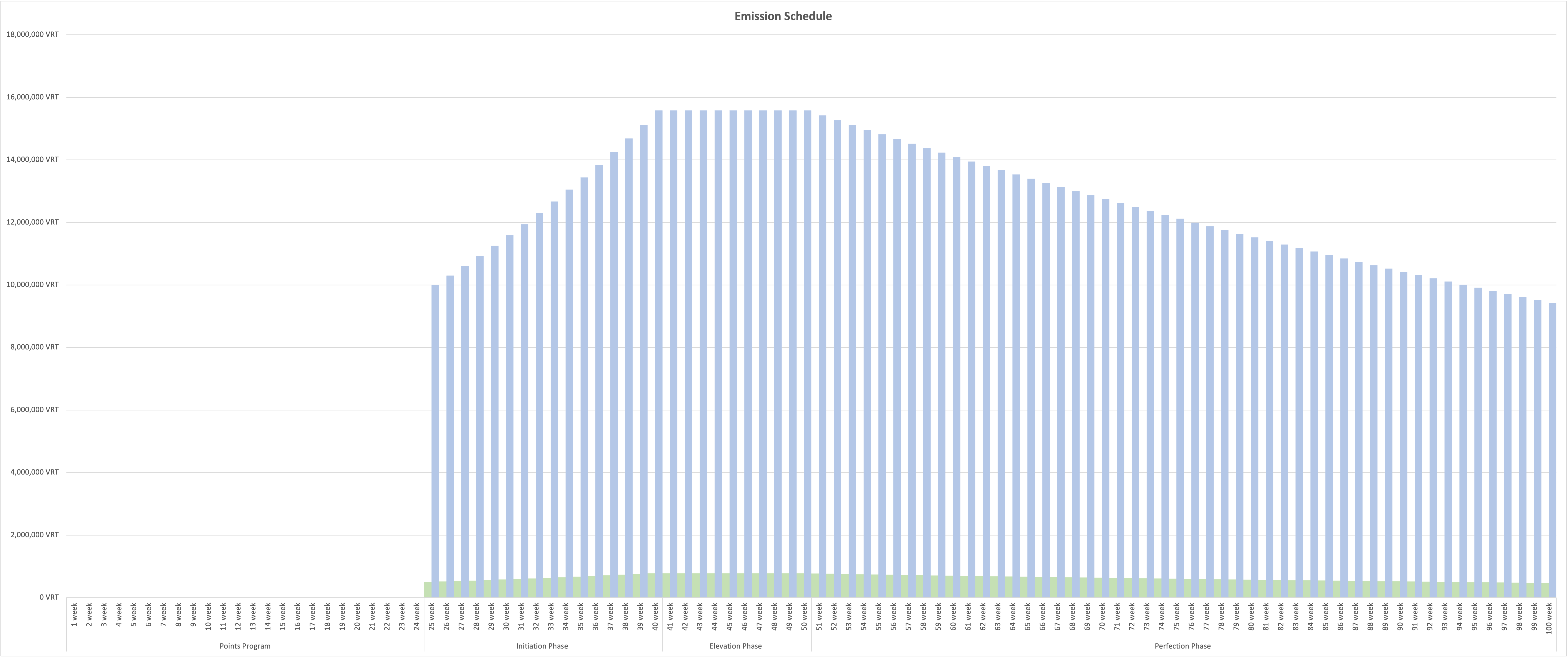

| 4 | Supply inflation: Weekly emissions follow a predefined, programmatic schedule (Attachment 1) divided into three distinct phases: Initiation, Elevation, and Perfection. During the Initiation Phase (weeks 25–40), weekly emissions start at 10,000,000 VRT and increase progressively with a weekly coefficient of 1.03 (3%), establishing the emission curve and accelerating supply growth to support early network participation. The Elevation Phase (weeks 41–50) represents the peak emission period. During this phase, weekly emissions stabilize at their maximum level with a coefficient of 1.0, maintaining strong incentives as the ecosystem reaches operational maturity. In the Perfection Phase (weeks 51–∞), emissions enter a controlled decline, decreasing gradually with a weekly coefficient of 0.99 (1%) to reinforce long-term sustainability and supply discipline. This structure results in a continuous, unlimited expansion of the VRT supply, distributed exclusively by smart contracts. Participants should consider this dynamic when evaluating their positions, as non-locked VRT holdings are subject to relative dilution against the expanding supply. |

| 5 | Liquidity fragmentation: VRT liquidity exists across multiple pool types (volatile, stable, concentrated) with varying fee tiers. This distribution can increase trading costs for larger transactions and complicate price discovery. Liquidity may shift between pools based on weekly voting outcomes. |

| 6 | Ecosystem correlation: VRT's value correlates strongly with Base blockchain adoption and success. Performance depends on Base's ability to attract and retain users, TVL, and developer activity relative to other Layer 2 solutions. |

| 7 | Functionality requirements: Protocol benefits such as voting rights and fee distribution require locking VRT as veVRT. Liquid token holders should understand they cannot directly participate in governance or earn protocol fees without locking. |

| 8 | Technical learning curve: Full protocol participation requires understanding epoch timing (weekly), voting mechanics, lock durations (1 week to 4 years), and rebase calculations. The rebase formula rewards veVRT holders based on the locked versus liquid ratio. |

| 9 | Lock-up considerations: veVRT positions involve time commitments ranging from 1 week to 4 years. Longer locks provide more voting power but reduce liquidity flexibility. While veVRT NFTs can be transferred, secondary market liquidity for these positions may be limited. |

I.4 Project Implementation-Related Risks

| # | Content |

|---|---|

| 1 | Base ecosystem dependency: VIRTUS Protocol's performance is tied to Base blockchain's success. If Base fails to attract sufficient users, developers, or TVL compared to competing Layer 2 solutions, VIRTUS Protocol would be negatively impacted regardless of its own merits or execution quality. |

| 2 | Emission sustainability risks: The protocol relies on VRT token emissions for growth, starting at 10,000,000 VRT weekly. As emissions decrease over time, there's risk that liquidity providers may withdraw if trading fee revenue does not adequately replace emission rewards, potentially creating a liquidity crisis. |

| 3 | Governance participation risks: Low veVRT holder engagement in weekly voting could result in poor emission allocation decisions or governance capture by small groups. Voter apathy may prevent the protocol from adapting effectively to market changes. |

| 4 | Inefficient capital allocation: Vote-buying through incentives may direct emissions to low-volume pools that offer high bribes rather than productive trading pairs. Short-term focused liquidity providers may extract value without contributing to long-term protocol health. |

| 5 | User adoption barriers: The complexity of epochs, voting mechanics, and dual-token system may limit adoption primarily to experienced DeFi users. This technical barrier could prevent the protocol from achieving mainstream adoption necessary for long-term success. |

| 6 | Liquidity fragmentation: Multiple pool types and fee tiers may spread liquidity too thin, resulting in poor trading conditions across many pairs rather than deep liquidity in key markets. New pairs may struggle to reach viable liquidity levels. |

| 7 | Partnership execution risks: Dependencies on third-party integrations and collaborations introduce risks outside VIRTUS Protocol's control. Failed integrations, partner protocol exploits, or misaligned incentives could negatively impact growth plans. |

I.5 Technology-Related Risks

| # | Content |

|---|---|

| 1 | Smart contract risks: While based on audited Velodrome V2 code, any smart contract system carries inherent risks. Potential issues could include unexpected interactions between components, edge cases in complex calculations, or unforeseen attack vectors as the protocol evolves. |

| 2 | Price oracle design: The 30-minute TWAP (Time-Weighted Average Price) balances manipulation resistance with price responsiveness. In pools with lower liquidity, sustained buying or selling pressure could theoretically influence price feeds, though this would require significant capital and time commitment. |

| 3 | Blockchain interactions: Users may encounter MEV (Maximum Extractable Value) common to all DEXs, including transaction ordering effects and arbitrage. These are inherent to public blockchain operations rather than protocol-specific issues. |

| 4 | Protocol interconnections: VIRTUS Protocol is designed to integrate with multiple decentralized finance protocols to support incentive mechanisms and ecosystem-level integrations. |

| 5 | This composability, while enabling rich functionality, means the protocol could be affected by issues in connected systems. |

| 6 | Upgrade processes: Governance-controlled upgrades allow protocol evolution but require active community oversight. The protocol includes timelocks and other safety mechanisms to protect against hasty changes. |

| 7 | Cross-chain operations: Assets bridged to Base use standard bridge infrastructure. While bridge technology has improved significantly, users should understand general cross-chain risks and only bridge amounts they're comfortable with. The VIRTUS Multichain Swapper facilitates these operations. |

| 8 | Access management: Users maintain full custody but must secure their private keys. Loss of wallet access means inability to access funds, as is standard for all non-custodial protocols. |

| 9 | Network capacity: During periods of high demand, Base network congestion could increase transaction costs or delays. The network continues to optimize for better performance and scalability. |

I.6 Mitigation Measures

| # | Content |

|---|---|

| 1 | Governance alignment through Auto Max-Lock: The VIRTUS Protocol's 100,000,000 VRT allocation is locked under the maximum lock duration ("Max Lock" mode), with the lock period continuously extended to maintain a permanent lock status. During the lock period, these tokens cannot be sold or transferred and may only be used for governance participation, ensuring alignment with the Protocol's long-term sustainability and success. |

| 2 | Inherited security architecture: Protocol built on Velodrome V2's extensively audited codebase, with Spearbit's audit identifying and resolving 1 critical and 8 high-risk issues before deployment that were resolved, providing proven security foundation. |

| 3 | Active bug bounty program: Continuous security incentives for white-hat researchers to identify vulnerabilities before malicious exploitation. |

| 4 | Emergency response capabilities: Emergency Council (0xC9C0608F551aDe53f911ceC50F565dB55c5bAFd1) a designated governance-controlled smart contract role is authorized to intervene during critical situations and can intervene to kill or revive gauges and set custom pool names/symbols during critical situations. |

| 5 | Multi-layered technical safeguards: The protocol implements defense-in-depth security through multiple mechanisms. Price manipulation is deterred through 30-minute Time-Weighted Average Price (TWAP) oracles that require attackers to maintain artificial prices for extended periods, making attacks economically unfeasible. Administrative functions are protected by multi-signature requirements preventing any single party from making unilateral changes. Core contracts are immutable once deployed, eliminating risks of malicious upgrades or rug pulls while allowing peripheral components to be upgraded through governance for necessary improvements. |

| 6 | Comprehensive economic protection: The protocol's economic design inherently protects against various attack vectors and misaligned incentives. The vote-locking mechanism allows participants to lock VRT for periods ranging from one week to four years, with voting power proportional to lock duration, ensuring those with the most influence have long-term alignment. The rebase mechanism, calculated as: weeklyEmissions × (1 - veVRT.totalSupply ÷ VRT.totalSupply)² × 0.5, automatically rewards veVRT holders more when locking participation decreases, creating a self-balancing incentive system. After approximately epoch 100, the VRT Fed activates, transferring monetary policy control to veVRT voters who can adjust emissions by ±0.01% of total supply per epoch through democratic voting, with hard bounds between 0.01% and 1% weekly preventing both hyperinflation and deflation. |

| 7 | Progressive decentralization pathway: While VIRTUS Protocol inherits decentralized architecture, the broader ecosystem continues to evolve. Base blockchain currently operates with a centralized sequencer, which is standard for Optimistic Rollups in their current stage of development. The Emergency Council provides specific intervention capabilities limited to pausing/reviving gauges and setting pool identifiers during the protocol's early stages. Over time, protocol control increasingly shifts to veVRT holders as the community demonstrates effective governance participation and the system proves its resilience. |

| 8 | Radical transparency and monitoring: All protocol operations occur on-chain, providing complete transparency and auditability. Every vote, emission distribution, fee allocation, and parameter change is permanently recorded on the Base blockchain and accessible through block explorers. The open-source codebase allows anyone to verify protocol behavior matches its documentation. Community members can access real-time analytics through various dashboards tracking TVL, volume, emissions, and voting patterns. Regular governance forums and community calls ensure open communication between the Foundation, developers, and token holders about protocol development and challenges. |

| 9 | Legal structure flexibility: Protocol structure designed to adapt to regulatory requirements while maintaining protocol operation and decentralization objectives. |

| 10 | Ecosystem integration: Strong connections with Base ecosystem and established DeFi protocols provide network effects and mutual support during challenges. |

Part A - Information about the offeror or the person seeking admission to trading

| # | Field | Content |

|---|---|---|

| A.1 | Name | VIRTUS Protocol |

| A.2 | Legal form | Not applicable |

| A.3 | Registered address | Not applicable |

| A.4 | Head office | Not applicable |

| A.5 | Registration Date | Not applicable |

| A.6 | Legal entity identifier | Not applicable |

| A.7 | Another identifier required pursuant to applicable national law | Not applicable |

| A.8 | Contact telephone number | Not applicable |

| A.9 | E-mail address | VirtUsProtocol@proton.me |

| A.10 | Response Time (Days) | Fourteen (14) days |

| A.11 | Parent Company | Not applicable |

| A.12 | Members of the Management body | Not applicable |

| A.13 | Business Activity | Supporting the development, maintenance and ecosystem growth of the VIRTUS Protocol decentralized exchange protocol. |

| A.14 | Parent Company Business Activity | Not applicable |

| A.15 | Newly Established | Not applicable |

| A.16 | Financial condition for the past three years | VIRTUS Protocol follows a capital-efficient and scalable operational model, prioritizing sustainable growth and long-term value creation. While current operations focus on core development and protocol stability, additional funding will be directed toward accelerating ecosystem expansion, regulatory readiness for VRT token trading, and broader market adoption. |

| A.17 | Financial condition since registration | Financial Position: The Protocol operates under a disciplined and capital-efficient model. Current resources include 100,000,000 VRT held in "Max Lock" mode as protocol-managed assets, which are allocated and locked to support development, infrastructure, and ecosystem operations. Ongoing protocol-level inflows are primarily derived from protocol-defined emission allocations, representing a 5% share of weekly VRT emissions, as well as fees generated by the VIRTUS Multichain Swapper. These inflows are designated to sustain core operations and support long-term ecosystem development. Monthly operating expenses primarily cover development team compensation and essential infrastructure costs. This lean cost structure enables the Protocol to prioritize long-term development objectives while maintaining a sustainable operational runway. Operational Performance: Key milestones achieved include the successful launch of the Protocol on the Base blockchain in February 2026, the implementation of the three-phase emission schedule, and ongoing preparation for MiCA-compliant admission to trading. The Protocol has demonstrated effective execution through consistent protocol operation and timely delivery of planned features. Ecosystem Growth: The Protocol has established the core operational infrastructure required to support the VIRTUS Protocol ecosystem, including technical partnerships for protocol development and preparation for future integrations with key decentralized finance protocols on Base. A 5% share of weekly VRT emission allocations is designated to fund ongoing development efforts and provide sustained support for ecosystem operations. These resources enable the Protocol to iteratively expand functionality while maintaining operational continuity. Strategic initiatives are focused on increasing protocol adoption, strengthening liquidity depth across supported trading pairs, and fostering long-term ecosystem resilience through targeted integrations and incentive alignment. |

Part D - Information about the crypto-asset project

| # | Field | Content |

|---|---|---|

| D.1 | Crypto-asset project name | VIRTUS Protocol |

| D.2 | Crypto-assets name | VIRTUS |

| D.3 | Abbreviation | VRT |

| D.4 | Crypto-asset project description | VIRTUS Protocol is a next-generation automated market maker (AMM) designed to serve as Base blockchain's central liquidity hub. The protocol combines a powerful liquidity incentive engine, vote-lock governance model, and user-friendly interface. Launched on March, 2026, it enables efficient token swaps through innovative pool designs and incentive mechanisms. |

| D.5 | Details of all natural or legal persons involved in the implementation of the crypto-asset project | The legal person involved in the implementation of the crypto-asset project is the VIRTUS Protocol, the details of which are provided under Part A. |

| D.6 | Utility Token Classification | FALSE |

| D.7 | Key Features of Goods/Services for Utility Token Projects | Not applicable |

| D.8 | Plans for the token | VRT will continue to serve as the VIRTUS Protocol's core governance and incentive token through a carefully designed three-phase emission framework. The Protocol has successfully completed the Initiation Phase (weeks 25–40), during which weekly token emissions increased progressively with a weekly coefficient of 1.03 (3%), supporting early liquidity bootstrapping and ecosystem formation. The Elevation Phase (weeks 41–50) represents the peak emission period, during which weekly emissions are capped at a maximum level with a coefficient of 1.0, providing strong and stable incentives while the ecosystem reaches operational maturity. During the Perfection Phase (weeks 51–∞), weekly emissions are designed to gradually decline with a weekly coefficient of 0.99 (1%), to reinforce long-term sustainability and supply discipline. When weekly emissions reach 9 million VRT (expected between weeks 100 and 110), the Protocol transitions into the VRT Fed framework, enabling veVRT governance participants to perform fine-grained monetary adjustments within strict, protocol-enforced boundaries. This structure results in a continuous, unlimited expansion of the VRT supply, distributed exclusively by smart contracts. Participants should consider this dynamic when evaluating their positions, as non-locked VRT holdings are subject to relative dilution against the expanding supply. This innovative mechanism transfers monetary policy control directly to veVRT token holders, who can vote each week to: (1) Increase total emissions by 0.01% of the circulating supply, (2) Decrease emissions by 0.01%, or (3) Maintain current emission levels. This democratic approach ensures VRT emissions remain responsive to market conditions and protocol needs, with built-in safeguards preventing extreme changes (minimum 0.01%, maximum 1% of total supply per week). The long-term vision positions VRT as the primary liquidity coordination tool for the Base blockchain ecosystem. |

| D.9 | Resource Allocation | Not applicable |

| D.10 | Planned Use of Collected Funds or Crypto-Assets | Not applicable |

Part E - Information about the offer to the public of crypto-assets or their admission to trading

| # | Field | Content |

|---|---|---|

| E.1 | Public Offering or Admission to trading | Admission to Trading (ATTR) |

| E.2 | Reasons for Public Offer or Admission to trading | The purpose of admission to trading is to provide regulated market access for existing VRT token holders and to enhance secondary market liquidity through compliant trading venues operating under the MiCA regulatory framework. The admission to trading does not constitute a public offering or sale of tokens, and no funds are raised by the Protocol in connection with the admission process. |

| E.3 | Fundraising Target | Not applicable |

| E.4 | Minimum Subscription Goals | Not applicable |

| E.5 | Maximum Subscription Goal | Not applicable |

| E.6 | Oversubscription Acceptance | Not applicable |

| E.7 | Oversubscription Allocation | Not applicable |

| E.8 | Issue Price | Not applicable |

| E.9 | Official currency or any other crypto-assets determining the issue price | Not applicable |

| E.10 | Subscription fee | Not applicable |

| E.11 | Offer Price Determination Method | Not applicable |

| E.12 | Total Number of Offered/Traded Crypto-Assets | Unlimited |

| E.13 | Targeted Holders | Not applicable. |

| E.14 | Holder restrictions | Not applicable |

| E.15 | Reimbursement Notice | Not applicable |

| E.16 | Refund Mechanism | Not applicable |

| E.17 | Refund Timeline | Not applicable |

| E.18 | Offer Phases | Not applicable |

| E.19 | Early Purchase Discount | Not applicable |

| E.20 | Time-limited offer | Not applicable |

| E.21 | Subscription period beginning | Not applicable |

| E.22 | Subscription period end | Not applicable |

| E.23 | Safeguarding Arrangements for Offered Funds/Crypto-Assets | Not applicable |

| E.24 | Payment Methods for Crypto-Asset Purchase | Not applicable |

| E.25 | Value Transfer Methods for Reimbursement | Not applicable |

| E.26 | Right of Withdrawal | Not applicable |

| E.27 | Transfer of Purchased Crypto-Assets | Not applicable |

| E.28 | Transfer Time Schedule | Not applicable |

| E.29 | Purchaser's Technical Requirements | Not applicable |

| E.30 | Crypto-asset service provider (CASP) name | Not applicable (no CASP engaged for placement services) |

| E.31 | CASP identifier | Not applicable |

| E.32 | Placement form | Placement form (NTAV) *NTAV represents the net tangible asset value of the Protocol at the time of disclosure and is provided for informational purposes only. |

| E.33 | Trading Platforms name | Admission to trading is intended on decentralized exchanges (DEXs), with specific platforms to be determined at a later stage. |

| E.34 | Trading Platforms Market Identifier Code (MIC) | OEUR *MIC provided on a provisional basis. Specific decentralized trading venues will be identified prior to admission to trading. |

| E.35 | Trading Platforms Access | Access to trading, where applicable, may require user registration on supported trading platforms, in accordance with each platform's terms, conditions, and eligibility requirements. |

| E.36 | Involved costs | Trading fees, where applicable, are determined by the relevant trading platform and its operator, in accordance with the platform's applicable fee schedule and terms. |

| E.37 | Offer Expenses | Not applicable |

| E.38 | Conflicts of Interest | None |

| E.39 | Applicable law | At the present stage, the VIRTUS Protocol does not designate a governing jurisdiction. Any future legal structuring, if implemented, will be disclosed separately. |

| E.40 | Competent court | No specific court or jurisdiction is designated. As the VIRTUS Protocol operates in a decentralized and non-custodial manner without a registered legal entity, disputes are not subject to the exclusive jurisdiction of any national courts. |

Part F - Information about the crypto-assets

| # | Field | Content |

|---|---|---|

| F.1 | Crypto-Asset Type | Crypto-asset other than an asset-referenced token or e-money token |

| F.2 | Crypto-Asset Functionality | VRT functions as the cornerstone of VIRTUS Protocol's decentralized governance and incentive system. The token operates through a dual-token model where VRT represents liquid, transferable value, while veVRT (vote-escrowed VRT) unlocks governance participation and protocol rewards. Core Functions: (1) Governance Activation: VRT holders can lock their tokens for 1 week to 4 years, receiving veVRT NFTs with voting power proportional to lock duration. For example: 100 VRT locked for 4 years = 100 veVRT (maximum voting power), 100 VRT locked for 1 year = 25 veVRT (25% voting power), 100 VRT locked for 1 week = 1.56 veVRT (minimal voting power). (2) Emission Direction: veVRT holders vote weekly (Thursday 00:00 UTC to Wednesday 23:59 UTC) to allocate VRT emissions to specific liquidity pools. This voting mechanism allows the community to incentivize liquidity where it's most needed. (3) Fee Distribution: Voters earn 100% of trading fees from pools they vote for, creating direct alignment between voting decisions and economic rewards. Additionally, voters receive any external incentives (bribes) deposited by protocols seeking liquidity. (4) Rebase Rewards: The protocol distributes additional VRT to veVRT holders through a rebase mechanism calculated as: Weekly Rebase = Weekly Emissions × (1 - veVRT Supply ÷ VRT Supply)² × 0.5. This formula rewards users who lock tokens when overall locking participation is low, creating a self-balancing incentive system. (5) Liquid Utility: VRT tokens maintain full ERC-20 functionality for trading, liquidity provision, and DeFi integrations, though governance and fee-earning privileges require locking. All functionalities have been operational since launch on March, 2026, executing autonomously through immutable smart contracts. |

| F.3 | Planned Application of Functionalities | All functionalities are currently operational. |

A description of the characteristics of the crypto-asset, including the data necessary for classification of the crypto-asset white paper in the register referred to in Article 109 of Regulation (EU) 2023/1114, as specified in accordance with paragraph 8 of that Article

| # | Field | Content |

|---|---|---|

| F.4 | Type of white paper | OTHR |

| F.5 | The type of submission | NEWT |

| F.6 | Crypto-Asset Characteristics | Overview: VRT is a standard ERC-20 token operating on Base, an Ethereum Layer 2 blockchain that provides faster and cheaper transactions while maintaining Ethereum's security guarantees. The token serves as the foundation for VIRTUS Protocol's decentralized exchange protocol. Technical Specifications: The VRT token contract (0x1CEFF1D2e0F0f0E27417C5600758EEc1606575CA) implements the complete ERC-20 standard, ensuring compatibility with all wallets, exchanges, and DeFi applications that support Ethereum-based tokens. The token uses 18 decimal places, matching Ethereum's native precision standard, allowing transactions as small as 0.000000000000000001 VRT. At launch, 200 million VRT tokens were created through a one-time minting event, with no capability for arbitrary future minting - all subsequent supply increases occur only through the protocol's transparent weekly emission schedule. Functional Properties: Each VRT token is completely fungible, meaning every token is identical and interchangeable with any other VRT token. The token contract includes no transfer restrictions, pause functions, or blacklist capabilities, ensuring censorship-resistant transfers between any addresses. Users benefit from Base's efficient infrastructure, with typical transaction costs of $0.01-0.05 and confirmation times of approximately 2 seconds, making VRT practical for both large and small transactions. Economic Characteristics: VRT exists purely as a digital asset with no physical representation or underlying collateral. Its value is determined entirely by market forces - supply and demand dynamics on exchanges and within the VIRTUS Protocol itself. The token provides no redemption rights against the issuer for fiat currency or other assets, functioning instead as a governance and incentive mechanism within the protocol. Token holders should understand that VRT's price can fluctuate significantly based on protocol usage, market sentiment, and broader cryptocurrency market conditions. Design Philosophy: The VRT token deliberately maintains a simple, secure design without complex features that could introduce vulnerabilities or unexpected behaviors. This minimalist approach ensures maximum compatibility with existing infrastructure while reducing potential attack vectors, making VRT a reliable foundation for the VIRTUS Protocol ecosystem. |

| F.7 | Commercial name or trading name | VRT |

| F.8 | Website of the issuer | https://virtus-protocol.com/ |

| F.9 | Starting date of offer to the public or admission to trading | 05/03/2026 |

| F.10 | Publication date | 05/03/2026 |

| F.11 | Any other services provided by the issuer | The Issuer does not provide any crypto-asset services covered by Regulation (EU) 2023/1114. |

| F.12 | Identifier of operator of the trading platform | Not applicable |

| F.13 | Language or languages of the white paper | English |

| F.14 | Digital Token Identifier Code used to uniquely identify the crypto-asset or each of the several crypto assets to which the white paper relates, where available | Not applicable |

| F.15 | Functionally Fungible Group Digital Token Identifier, where available | Not applicable |

| F.16 | Voluntary data flag | FALSE |

| F.17 | Personal data flag | FALSE |

| F.18 | LEI eligibility | Not available |

| F.19 | Home Member State | Not available |

| F.20 | Host Member States | Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden. |

Part G - Information on the rights and obligations attached to the crypto-assets

| # | Field | Content |

|---|---|---|

| G.1 | Purchaser Rights and Obligations | VRT token holders possess the right to freely transfer their tokens as standard ERC-20 assets without any restrictions, lock their VRT for periods ranging from one week to four years to receive veVRT NFTs in proportion to their lock duration, and participate in the protocol's ecosystem through liquidity provision or trading activities. However, VRT tokens alone do not confer governance voting rights, fee distribution claims, or any direct protocol control, as these privileges are reserved for veVRT holders. VRT holders are obligated to bear all transaction costs associated with transfers and protocol interactions, understand the distinction between VRT and veVRT functionalities, comply with applicable laws and regulations in their jurisdiction, and accept full responsibility for the security of their tokens including private key management. Holders must also understand that VRT is subject to ongoing supply inflation through weekly emissions, which may dilute their proportional ownership unless they participate in the veVRT locking mechanism to receive rebases. |

| G.2 | Exercise of Rights and Obligations | To begin using VRT tokens, holders need a Web3-compatible wallet connected to the Base network. Holders must ensure their wallet contains sufficient ETH to cover transaction fees, which typically range from $0.01 to $0.05 per transaction. Basic token transfers follow the standard ERC-20 process - holders simply input the recipient address and amount, then confirm the transaction. Converting VRT to veVRT for Governance: To participate in protocol governance and earn fees, VRT holders can lock their tokens through the VotingEscrow-contract (0x6Be687DF2ab94fBD7Eeb4dAc32118110967FF0ef). The process is straightforward: holders visit the VIRTUS interface, select their desired lock duration (1 week minimum, 4 years maximum), and confirm the transaction. The system calculates the veVRT amount using a simple formula: the VRT amount multiplied by the lock duration as a percentage of the maximum 4 years. For example, locking 1,000 VRT for 2 years yields 500 veVRT (50% of maximum), while locking for the full 4 years yields the full 1,000 veVRT. Active Participation in Governance: Once holding veVRT, token holders can participate in weekly voting cycles that run from Thursday 00:00 UTC to Wednesday 23:59 UTC. During each cycle, veVRT holders allocate their voting power to liquidity pools they want to support - these pools will receive VRT emissions proportional to votes received. In return for voting, veVRT holders earn 100% of trading fees generated by their chosen pools, plus any incentives deposited by protocols seeking liquidity. Rewards accumulate continuously and can be claimed at any time. Additionally, all veVRT holders receive automatic weekly rebases that increase their veVRT balance. Managing Locked Positions: veVRT positions offer flexibility within their lock constraints. Holders can add more VRT to an existing lock at any time, increasing their veVRT balance and potentially extending their lock period. The "Max Lock" mode feature automatically maintains positions at the maximum 4-year lock, ensuring consistent maximum voting power. When lock periods expire, holders can withdraw their original VRT tokens. While locked VRT cannot be withdrawn early, the veVRT NFT itself can be transferred between wallets, allowing position management across different addresses. All these functions are available 24/7 through the VIRTUS Protocol interface at https://virtus-protocol.com/ other third-party interfaces, or via direct smart contract interaction for advanced users. |

| G.3 | Conditions for Modifications of Rights and Obligations | Governance Structure: The VIRTUS Protocol operates under a decentralized governance model where only veVRT holders - those who have locked their VRT tokens - can propose and vote on changes. This design ensures that decision-makers have long-term skin in the game, as their tokens remain locked during the governance process. VRT holders who wish to participate in governance must first lock their tokens, with voting power proportional to both the amount locked and the duration of the lock. Voting Process: Governance proposals follow a structured weekly cycle aligned with the protocol's epoch system (Thursday to Wednesday). When a proposal is submitted, veVRT holders can allocate their voting power to support or oppose the change. Decisions are made by simple majority of participating voting power, with no minimum quorum currently required. This streamlined approach enables responsive governance while preventing small holders from blocking necessary updates. Approved changes typically take effect in the following epoch, providing participants time to adjust their strategies. Emergency Interventions: The protocol maintains an Emergency Council (0xC9C0608F551aDe53f911ceC50F565dB55c5bAFd1) with strictly limited powers for critical situations. This council can pause or resume specific liquidity pool gauges if technical issues arise, and can update pool names or symbols for clarity. Importantly, the council cannot modify core token economics, access user funds, or make changes to fundamental protocol rules. These constraints ensure emergency powers cannot be abused while still providing necessary tools for crisis management. Scope and Limitations: Through governance, veVRT holders can modify various protocol parameters including emission rates (after the VRT Fed activates around epoch 100-110), trading fee structures, gauge weights for liquidity pools, and integration of new pool types or features. However, certain elements remain immutable by design. The core VRT token contract itself cannot be modified, ensuring token holders' fundamental rights remain protected. This immutability provides certainty about basic token properties while allowing the protocol to evolve through peripheral upgrades. Participation Requirements: The governance system intentionally favors long-term aligned participants. A user locking tokens for 4 years has 4 times the voting power of someone locking for 1 year, ensuring those with the greatest long-term exposure have proportionally greater influence. This mechanism naturally filters governance participation to users genuinely involved in the protocol's long-term success rather than short-term speculators. |

| G.4 | Future Public Offers | No public offers have been conducted for the VRT token, and no future public offers are planned. Early users of the Protocol were able to participate in a time-limited Points Program, designed solely to incentivize protocol usage and user activity. Participation in the Points Program did not constitute a public offer, token sale, or fundraising event. |

| G.5 | Issuer Retained Crypto-Assets | At launch, the VIRTUS Protocol retained 100,000,000 VRT tokens, representing 50% of the initial 200M supply, Minted to the "Operation Wallet"). These tokens are subject to an immediate and mandatory "Max Lock" veVRT lock-up, implemented at launch, ensuring permanent maximum voting power without decay. Additionally, the Protocol receives 5% of all weekly emissions on an ongoing basis to fund continued development, maintenance, and operational expenses. |

| G.6 | Utility Token Classification | FALSE |

| G.7 | Key Features of Goods/Services of Utility Tokens | Not applicable |

| G.8 | Utility Tokens Redemption | Not applicable |

| G.9 | Non-Trading request | TRUE |

| G.10 | Crypto-Assets purchase or sale modalities | Through compatible trading platforms, CASPs, or decentralized exchange protocols. |

| G.11 | Crypto-Assets Transfer Restrictions | None |

| G.12 | Supply Adjustment Protocols | Overview of the Three-Phase Emission System: The VIRTUS Protocol implements a structured and programmatic token emission framework designed to balance early growth incentives with long-term sustainability. Beginning with an initial emission allocation of 200,000,000 VRT, the Protocol follows a predetermined three-phase emission model, aligned with different stages of protocol maturity. Phase 1 - Initiation (Weeks 25-40): During the initial launch phase, the Protocol prioritized rapid liquidity formation and early user adoption. Weekly emissions began at 10,000,000 VRT in week 1, representing approximately 2.0% of the initial supply, and increased progressively with a weekly coefficient of 1.03 (3%), This accelerated growth phase was designed to incentivize early liquidity providers and bootstrap core trading pairs within the ecosystem and establish VIRTUS Protocol as Base's primary DEX. By week 40, weekly emissions reached approximately 15.6 million VRT, establishing sufficient liquidity depth to support sustainable protocol operations. Phase 2 - Elevation (Weeks 41 to Week 50): Following the completion of the Initiation Phase, the Protocol entered the Elevation Phase, representing the peak emission period. During this phase, weekly emissions are capped and stabilized at their maximum level with a coefficient of 1.0 per epoch. This stabilization phase maintains strong incentive alignment while enabling a smooth transition from growth-driven incentives toward longer-term sustainability mechanisms. The Elevation Phase continues until week 50, when emissions begin to transition into a controlled reduction path. Phase 3 - Perfection (weeks 51 to ∞): The emissions enter a controlled decline, decreasing gradually with a weekly coefficient of 0.99 (1%) to reinforce long-term sustainability and supply discipline. Gradually reducing inflation while maintaining attractive yields for liquidity providers. This phase continues until emissions naturally decay to 9.5 million VRT per week, expected around epoch 100-110. The gradual reduction ensures a smooth transition from growth-focused incentives to fee-based sustainability. The most innovative aspect of VIRTUS Protocol's tokenomics activates when emissions fall below 9.5 million VRT weekly. At this point, monetary policy control transfers directly to veVRT holders through the "VRT Fed" mechanism (VRT Fed Weeks 100~110). Each week, voters can choose to: increase emissions by 0.01% of total supply (adding additional 50K-100K VRT depending on epoch supply), decrease emissions by 0.01%, or maintain the current level. The winning option is determined by simple majority vote, with changes taking effect one epoch later. This democratic approach ensures emissions can respond to market conditions while hard-coded boundaries (minimum 0.01%, maximum 1% of total supply per week) prevent extreme monetary policy decisions. Initial Token Distribution: Of the 200 million initial tokens, 100 million were distributed as locked veVRT positions to early supporters and partners, ensuring long-term alignment. The remaining 100 million entered circulation as liquid VRT supporting market activity, liquidity provisioning, and protocol usage. This distribution model created immediate governance participation while maintaining sufficient liquid supply for market operations. The VIRTUS Protocol's 5% share of ongoing emissions provides sustainable development funding without requiring token sales. |

| G.13 | Supply Adjustment Mechanisms | Distribution Mechanisms: (1) Liquidity Provider Rewards (Primary Distribution): Weekly VRT emissions flow to liquidity pools based on veVRT voting allocation. Liquidity providers stake LP tokens in gauges to earn emissions. Distribution is proportional to share of liquidity in the pool and percentage of veVRT votes the pool receives. Rewards are claimable continuously as they accrue. (2) Rebase Mechanism (veVRT Holder Rewards): Formula: Weekly Rebase = Weekly Emissions × (1 - veVRT Supply ÷ VRT Supply)² × 0.5. How it works: If 50% of VRT is locked as veVRT: Rebase = Emissions × 0.125. If 25% of VRT is locked as veVRT: Rebase = Emissions × 0.28125. Lower lock percentage = Higher rebase rewards. Distribution: Proportional to each user's veVRT balance. Purpose: Incentivizes locking when participation is low. (3) Automatic Execution: Minter Contract: 0xDc1dE416DdaD4c9e8328F30aE88E2392d5b551f7 Executes distributions at epoch boundaries (Thursdays 00:00 UTC). No manual intervention required. All calculations performed on-chain for transparency. (4) Team Allocation: 5% of weekly emissions automatically directed to VIRTUS Protocol ("Operation Wallet"). Used for development, maintenance, and ecosystem growth. Provides sustainable funding without token sales. Example Weekly Distribution (10M VRT emission): 9.5M VRT: To liquidity pools based on votes. 0.5M VRT: To VIRTUS Protocol (5%). Additional rebase: Calculated based on lock ratio. This mechanism ensures efficient capital allocation while rewarding both liquidity providers and long-term token holders. |

| G.14 | Token Value Protection Schemes | Not applicable |

| G.15 | Token Value Protection Schemes Description | FALSE |

| G.16 | Compensation Schemes | FALSE |

| G.17 | Compensation Schemes Description | Not applicable |

| G.18 | Applicable law | At the present stage, the VIRTUS Protocol does not designate a governing jurisdiction. Any future legal structuring, if implemented, will be disclosed separately. |

| G.19 | Competent court | No specific court or jurisdiction is designated. As the VIRTUS Protocol operates in a decentralized and non-custodial manner without a registered legal entity, disputes are not subject to the exclusive jurisdiction of any national courts. |

Part H – Information on the underlying technology

| # | Field | Content |

|---|---|---|

| H.1 | Distributed ledger technology | VRT operates on Base blockchain, which is an Ethereum Layer 2 scaling solution using Optimistic Rollup technology. |

| H.2 | Protocols and technical standards | The protocol utilizes ERC-20 standard for VRT tokens (fungible tokens), ERC-721 standard for veVRT NFTs (non-fungible tokens representing locked positions), and Ethereum-compatible smart contracts following Solidity best practices. |

| H.3 | Technology Used | VIRTUS Protocol is built on Base blockchain, an Ethereum Layer 2 network. The protocol consists of a system of smart contracts written in Solidity that implement automated market maker functionality. The core technology includes decentralized exchange smart contracts for token swapping, liquidity pool contracts for asset management, governance contracts for protocol decision-making, and reward distribution contracts for incentive allocation. All contracts are deployed on Base's distributed ledger and interact through standardized interfaces. |

| H.4 | Consensus Mechanism | VRT tokens operate on Base, which uses Optimistic Rollup technology rather than a traditional consensus mechanism. Base processes transactions off-chain and periodically submits transaction batches to Ethereum mainnet, relying on Ethereum's Proof-of-Stake consensus for final settlement and security. |

| H.5 | Incentive Mechanisms and Applicable Fees | How VIRTUS Rewards Participants: The protocol operates on a simple principle: every participant should be fairly compensated for their contribution. Unlike traditional exchanges that extract value through fees, VIRTUS Protocol returns 100% of trading fees to veVRT voters, creating a truly community-owned marketplace. Liquidity Provider Rewards: Liquidity providers form the backbone of any DEX, and VIRTUS Protocol ensures they are well compensated. Each week, the protocol distributes VRT emissions to liquidity pools based on veVRT holder votes. Providers earn these rewards proportionally based on their share of each pool. There are no minimum requirements - whether providing $100 or $1 million in liquidity, rewards are distributed fairly based on proportional contribution. Providers simply stake their LP tokens in the appropriate gauge and rewards accumulate automatically. Trading Fee Structure: Different pool types charge different fees optimized for their use cases. Stable pools (for correlated assets like USDC/USDT) typically charge 0.01-0.05%, minimizing costs for traders swapping between similar assets. Volatile pools (for uncorrelated assets like ETH/USDC) generally charge 0.30%, reflecting the higher risk and impermanent loss potential. Concentrated liquidity pools feature variable fees based on the selected price range. Importantly, the protocol itself retains none of these fees - 100% flows to veVRT voters who supported those specific pools. Vote Incentives Marketplace: One of VIRTUS Protocol's most innovative features is the vote incentive system, often called "bribes." External protocols can deposit incentives (in any ERC-20 token) to attract veVRT votes to their pools. This creates an efficient marketplace where protocols can bootstrap liquidity without selling tokens. Voters who allocate to incentivized pools receive these rewards in addition to trading fees, often making certain pools particularly attractive. This system has proven highly effective at directing liquidity where it's most needed. Network Operating Costs: Users pay Base blockchain transaction fees in ETH for all operations. Thanks to Base's efficient Layer 2 architecture, these costs typically range from $0.01-0.05 per transaction - a fraction of Ethereum mainnet costs. These fees go to the Base network, not to VIRTUS Protocol. The protocol itself imposes no additional charges for deposits, withdrawals, or any other operations. Sustainable Development Funding: Rather than relying on venture capital or token sales, VIRTUS Protocol funds ongoing development through a 5% allocation of weekly emissions to the VIRTUS Protocol. This aligns team incentives with protocol growth - the team only benefits when the protocol succeeds. This sustainable model ensures continuous development without extracting value from users or requiring external funding. |

| H.6 | Use of Distributed Ledger Technology | FALSE |

| H.7 | DLT Functionality Description | Base operates as an Optimistic Rollup Layer 2 that processes transactions off Ethereum mainnet while inheriting its security. Transactions are executed on Base with near-instant confirmation (blocks every 2 seconds), then batched and compressed by sequencers before being posted to Ethereum as calldata or blobs. This batching significantly reduces costs as users share gas fees across all bundled transactions. The "optimistic" model assumes all transactions are valid unless challenged during a 7-day dispute window, during which anyone can submit fraud proofs to revert invalid transactions. This architecture enables VRT tokens and VIRTUS Protocol operations to achieve high speed and low costs while maintaining Ethereum's security guarantees, with all data remaining publicly verifiable on both Base and Ethereum blockchains. |

| H.8 | Audit | VIRTUS Protocol inherits its contract architecture from Velodrome V2, which has been audited by reputable security firms (Spearbit, Chainsecurity, Code4Rena, and Sherlock). The protocol maintains an active bug bounty program for ongoing security. |

| H.9 | Audit outcome | The Velodrome V2 protocol, from which VIRTUS Protocol inherits its codebase, underwent comprehensive security review by Spearbit over 10 days in February-March 2023. The audit identified 119 issues across all severity levels: 1 critical risk (fixed), 8 high risks (all fixed), 19 medium risks (16 fixed, 3 acknowledged), 30 low risks (18 fixed, 12 acknowledged), and 61 gas optimization/informational items. The critical and all high-risk issues were resolved before deployment. Post engagement reviews were conducted in May and June 2023 to verify fixes. Aerodrome Security Page: (https://aerodrome.finance/security). The Pool Launcher module was audited by MixBytes between 12th September and 3rd October 2025. MixBytes Audit Report: (https://github.com/mixbytes/audits_public/tree/master/Velodrome/Pool%20Launcher) Pool Launcher Codebase: (https://github.com/velodrome-finance/pool-launcher) Contracts: (https://github.com/velodrome-finance/pool-launcher/tree/develop/deployment-addresses) |

Part J – Information on the sustainability indicators in relation to adverse impact on the climate and other environment-related adverse impacts

| # | Field | Content |

|---|---|---|

| J.01 | Name | VIRTUS Protocol - As issuer of VRT token operating on Base (Optimistic Rollup), environmental impacts relate to Ethereum's Proof-of-Stake consensus mechanism which provides final settlement and security for all Base transactions. |

| J.02 | Relevant legal entity identifier | Not Applicable |

| J.03 | Name of the crypto-asset | VIRTUS |

| J.04 | Consensus Mechanism | Optimistic Rollup (Base L2) settled on Ethereum Proof-of-Stake - Base has no independent consensus mechanism but relies on Ethereum's PoS for security and finality. |

| J.05 | Incentive Mechanisms and Applicable Fees | The VIRTUS Protocol operates without traditional mining or validation rewards since Base, as an Optimistic Rollup, does not require a separate consensus mechanism. Instead, the protocol's incentive structure consists of: (1) VRT token emissions distributed weekly to liquidity providers based on veVRT holder voting, starting at 10,000,000 VRT per week with programmatic adjustments, (2) Trading fees collected from each swap in Liquidity Pools, varying by pool type (stable, volatile, or concentrated liquidity), with 100% distributed to veVRT voters who allocated votes to those pools, (3) External incentives that can be deposited by third parties to attract votes to specific pools, and (4) Rebase rewards for veVRT holders calculated as a percentage of weekly emissions. Users pay Base network transaction fees in ETH for all operations, which are significantly lower than Ethereum mainnet fees due to transaction batching. The protocol itself retains no trading fees, with only 5% of VRT emissions directed to the team for ongoing development. |

| J.06 | Beginning of the Period to which the Disclosed Information Relates | 05/03/2026 |

| J.07 | End of the Period to which the Disclosed Information Relates | N/A |

Mandatory key indicator on energy consumption

| # | Field | Content |

|---|---|---|

| J.08 | Energy Consumption | Estimated 50,000-150,000 kWh annually. Energy calculations follow the Crypto Carbon Ratings Institute (CCRI) methodology adapted for Layer 2 networks. The assessment considers: (a) Base sequencer operations (estimated 100-200W based on server specifications), transaction batching efficiency (hundreds of transactions per Ethereum submission), and proportional allocation of Ethereum's settlement energy. (b) Using Ethereum's measured consumption of 4,410,000 kWh annually and Base's data posting frequency, VRT's share is estimated based on protocol activity, placing it at an estimated share of 0.1-0.5%. This methodology provides conservative estimates as Optimistic Rollups achieve significant efficiency through off-chain computation. |

Sources and methodologies

| # | Field | Content |

|---|---|---|

| J.09 | Energy Consumption Sources and Methodologies | The Crypto Carbon Ratings Institute (CCRI) methodology for PoS networks has been adapted for Layer 2 assessment. Energy calculations consider: (1) Base sequencer hardware requirements estimated at 100-200W based on high-performance server specifications comparable to CCRI's Configuration 5-6, (2) Transaction volume analysis with marginal power demand estimated at 0.01-0.05W per TPS, consistent with efficient PoS networks studied, (3) Layer 2 specific operations including batching, compression, and Ethereum data posting, (4) Carbon intensity using global average of 358 gCO2e/kWh per International Energy Agency (IEA) standards. According to the Cambridge Blockchain Network Sustainability Index (https://ccaf.io/cbnsi/ethereum), post-Merge Ethereum operates with best-guess power demand of 502.5 kW and annualized consumption of 4,420,000 kWh (4.42 GWh), representing a 99.95% reduction from pre-Merge levels. Furthermore, the emission intensity is approximately 358 gCO2e/kWh due to increasing renewable energy adoption. The Cambridge methodology incorporates real-time Beacon Node counts, consensus client distribution, and hardware configurations ranging from consumer-grade to high-performance servers, with power consumption validated through empirical measurements. Sustainable energy sources account for over 30% of Ethereum's electricity mix, including hydroelectric (15%), wind (12%), and solar (4%) power. VRT's share is allocated based on its proportion of Base network activity. This methodology provides conservative estimates, as Optimistic Rollup architecture achieves significant efficiency improvements through off-chain computation. |

| J.10 | Environmental Impact | Based on the adapted methodology using Cambridge Centre for Alternative Finance data, the VRT protocol's estimated annual carbon footprint ranges from 18 to 54 tonnes CO2 equivalent, calculated using Ethereum's current emission intensity of 358-396 gCO2e/kWh. According to Cambridge's data (https://ccaf.io/cbnsi/ethereum), Ethereum's post-Merge annual emissions are approximately 1.58 KtCO2e, representing a 99.95% reduction from its proof-of-work era. As a Layer 2 protocol, Base's emissions would be a small fraction of Ethereum's total, given that hundreds of L2 transactions are batched into single Ethereum submissions. VRT's share, as one protocol among many on Base, would represent an even smaller fraction. Using conservative estimates and the global carbon intensity factor of 358 gCO2e/kWh, VRT's estimated annual carbon footprint would likely range from 25 to 75 tonnes CO2 equivalent, depending on its share of Base network activity. This equals approximately 4-12 roundtrip flights Munich-San Francisco (6.1 tCO2e per flight). As Base infrastructure matures and the Ethereum validator network continues shifting toward renewable energy, carbon intensity is expected to improve further. |

ATTACHMENT 1 — Preliminary Emission Schedule

| Phases | Schedule | Avg per 1 week to Team | Avg per 1 week to Liquidity Providers | Δ Emission |

|---|---|---|---|---|

| Points Program | 1 week – 24 week | 0.00 VRT | 0.00 VRT | 0% |

| Initiation Phase | 25 week – 40 week | 630,000 VRT | 12,600,000 VRT | Coeff = 1.03/per week |

| Elevation Phase | 41 week – 50 week | 780,000 VRT | 15,600,000 VRT | Coeff = 1/per week |

| Perfection Phase | 51 week – ∞ week | 610,000 VRT (51-100 weeks) | 12,180,000 VRT (51-100 weeks) | Coeff = 0.99/per week |

ATTACHMENT 2 — Distribution Model

| Allocation | Token | Amount | Mint Phase | Wallet/Smart Contract | Action |

|---|---|---|---|---|---|

| Initial liquidity | VRT | 50 mln. | 1st | Smart Contract | Supplied in LP |

| Points Program Initial liquidity | PTS | 30 mln. | 1st | "Team Wallet" Safe | Free to use on "TW" |

| Grants to cover Points Program incentives and to fund external and internal contributors who expand the protocol's functionality, adoption, security, and integrations | VRT | 20 mln. | 1st | "Operational Wallet" Safe | Free to use on "OW" |

| Operations purpose | VRT | 100 mln. | 1st | "Operational Wallet" Safe | Locked for 4 years |

| Emission&Rewards | VRT | Unlimited | 2nd | Smart Contract | Manually Start of Mint upon completion of Points Program |

© 2026 VIRTUS Protocol. All rights reserved.